Taxes in Japan have a way of feeling like a black box you’re not allowed to look inside—money leaves your paycheck, forms arrive in Japanese, and nobody quite explains the logic. Then one year the box surprises you. When I registered my own business, the first year felt suspiciously light on tax. I assumed I’d simply gotten off easy. I hadn’t: the bill for that first year showed up the following June, and my second year is when the penny—and the invoice—dropped. That lag is the single most important thing to understand about tax here, and almost nobody tells you before it happens.

I’m Japanese, I run my own business, and I’ve fumbled through these forms myself—so this is the plain-English version I wish I’d had. We’ll cover the two taxes you actually pay, the timing trap that catches everyone, whether your overseas income is even taxable here, and when you have to file a return yourself. This is an overview to make the system make sense; for anything complex, a licensed zeirishi (tax accountant) is worth every yen.

The two taxes you’ll pay

Almost everyone living in Japan pays two separate taxes on their income, and confusing them is the root of most tax surprises:

- National income tax (所得税, shotokuzei) — paid to the central government, on a progressive scale from 5% up to 45% depending on how much you earn.

- Local residence tax (住民税, jūminzei) — paid to your city and prefecture, at a roughly flat 10%, plus a small fixed per-person amount.

The income tax is the one people expect. The residence tax is the one that ambushes them—because of when it’s charged. We’ll take them in turn.

Income tax: mostly handled for you

If you’re a company employee, income tax is quietly deducted from every paycheck—this is withholding (源泉徴収, gensen chōshū). Once a year, around November or December, your employer runs a year-end adjustment (年末調整, nenmatsu chōsei) that reconciles what was withheld against what you actually owe, applying your deductions. For most salaried people, that’s the entire process: you never file anything, and any small refund appears in your December or January pay.

The rate is progressive, applied in bands, so only the portion of income in each band is taxed at that band’s rate—earning more never leaves you worse off. A separate 2.1% reconstruction surtax rides on top of your income tax through 2037. If you’re self-employed or freelance, nothing is withheld for you; you calculate and pay it yourself through a tax return, which we’ll get to.

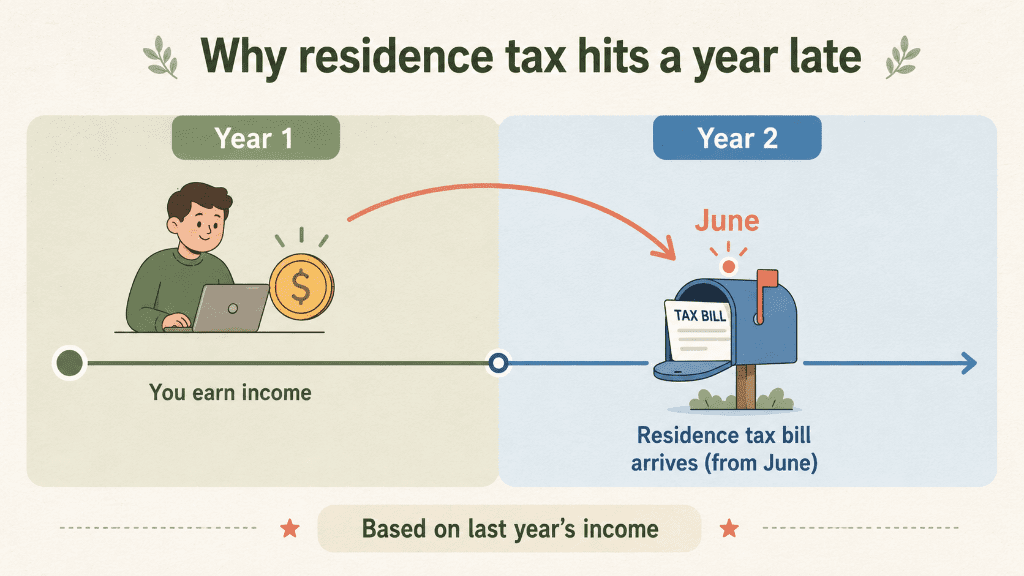

Residence tax: the year-two trap

Here’s the one to tattoo on your arm. Residence tax is charged on last year’s income, and billed the following year. It’s assessed based on where you were registered as living on January 1, calculated from your previous calendar year’s earnings, and collected starting the following June.

That one-year delay is why my first year in business felt cheap and my second year didn’t. It’s also why residence tax hurts most at exactly the wrong moments:

- Your first full year in Japan is often residence-tax-free, because there was no prior-year Japanese income to tax. Newcomers pocket that and then get startled in year two.

- When you quit, switch jobs, or go freelance, the bill keeps coming based on the good year you just left. People who stop working in, say, spring still owe residence tax on last year’s full salary—with no paycheck to draw it from.

- When your income drops, the tax doesn’t drop with it until the year after. Budget for the lag, not for this month’s reality.

How you pay depends on your status. Employees have it deducted from their salary in twelve installments from June through May (special collection, tokubetsu chōshū). Everyone else gets a set of payment slips (普通徴収, futsū chōshū) from the municipality in June, due in four installments across the year. The lesson every self-employed person learns once: set aside money for a tax that reflects last year, not this one.

Is your overseas income even taxable here?

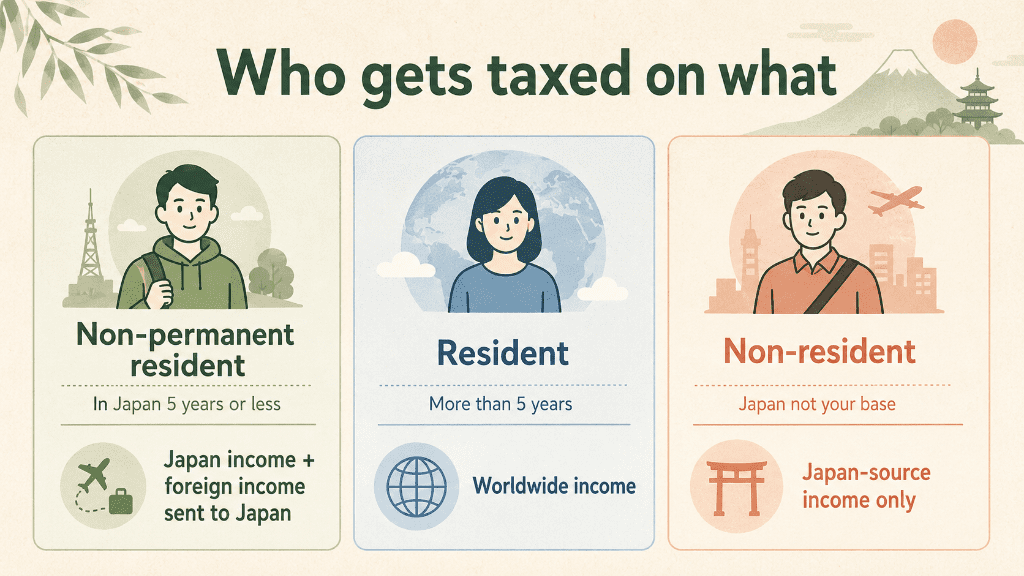

This is the question that matters most to newcomers with income or assets back home, and Japan’s answer is more generous than people assume—at least at first. Your tax status falls into one of three buckets:

- Non-permanent resident (非永住者): a non-Japanese national who has had a home in Japan for five years or less within the past ten. You’re taxed on your Japan-source income, plus any foreign income you actually pay into or remit to Japan. Foreign-source income that stays abroad and isn’t sent here is generally not taxed. This is the meaningful break for your first years.

- Permanent resident for tax (居住者): once you pass that five-year mark, you’re taxed on your worldwide income, remitted or not. (This “permanent” is a tax term—it has nothing to do with permanent-residency visa status.)

- Non-resident (非居住者): if Japan isn’t your base of life, you’re taxed only on income sourced in Japan.

The remittance rule has real teeth: for non-permanent residents, sending overseas earnings into Japan in the same year can pull them into the tax net. Japan also has tax treaties with many countries to prevent double taxation, and rules on foreign tax credits. If you have foreign salary, investments, rental property, or crypto, this is exactly the point to talk to a zeirishi—the official framing is on the National Tax Agency’s English pages.

When you have to file a return yourself (確定申告)

The final tax return (確定申告, kakutei shinkoku) is filed once a year, roughly February 16 to March 15, covering the previous calendar year. Most ordinary employees never touch it—their year-end adjustment does the job. You generally do need to file if you:

- Are self-employed, freelance, or run a business;

- Have side income over ¥200,000 in the year, or income over ¥20 million;

- Had two or more employers, or no year-end adjustment;

- Want to claim certain deductions—large medical expenses, a first-year mortgage, or furusato nozei without the one-stop shortcut.

You’ll need your My Number to file, and the process is increasingly doable online through the e-Tax system. Now the part I personally got wrong: after my first return, I assumed a payment slip would arrive in the mail later, the way the residence-tax bill does. It doesn’t. Income tax you calculate on your return is due by the same March 15 deadline, and you pay it yourself—by bank transfer, at a convenience store, by credit card, or by setting up account direct debit (振替納税, which conveniently pushes the date to around late April). Filing and paying are one event, not two. Residence tax is the one that comes later as a slip; don’t mix them up like I did.

Paying less: deductions and furusato nozei

Your tax is calculated on income after deductions, so knowing which apply to you is where the savings are. Beyond the basic and employment deductions everyone gets, common ones include dependents, spouse, social-insurance premiums (your pension and health-insurance payments are deductible), life insurance, large medical bills, and iDeCo pension contributions.

The most beloved trick, though, is furusato nozei—a program that lets you redirect part of your residence tax to regional towns and get local food and goods in return, for just a ¥2,000 out-of-pocket cost. It’s the rare case where doing your taxes comes with a box of crab in the mail. We break the whole thing down, including the income limits and the one-stop shortcut, in our guide to furusato nozei for foreign residents.

Changing jobs or leaving Japan: the bill that follows you

Because residence tax lags a year, leaving Japan doesn’t leave the tax behind. If you were a resident on January 1, you owe that year’s residence tax on last year’s income even if you fly home in March. Two things to arrange before you go:

- Appoint a tax representative (納税管理人, nōzei kanrinin)—a person or company in Japan who receives your tax slips and pays on your behalf after you leave. You file a simple notice with your ward office and tax office to name them. Without one, your bills have nowhere to go.

- Settle income tax before departure, either by filing an early return (準確定申告) yourself or leaving it to your representative. Employees changing jobs mid-year should also confirm how their remaining residence tax will be collected—lump-summed from a final paycheck, or switched to slips.

If you’re going the other direction—starting out on your own—the tax and paperwork of self-employment are their own world; our guide to starting a business in Japan as a foreigner picks up there.

What’s new: the 2025 “¥1.6 million wall”

Japan’s 2025 tax reform raised the point at which income tax kicks in. By lifting the basic deduction and the minimum employment-income deduction (to ¥650,000), the old ¥1.03 million tax-free line moved up to about ¥1.6 million for income tax, effective from the 2025 tax year. It mostly matters for part-time and dependent earners deciding how many hours to work. Two caveats worth knowing: this change is about income tax, so residence tax can still apply from around ¥1.1 million, and part of the relief is a temporary measure being reshaped again from 2027. As always with thresholds, check the current year’s figures before you plan around them.

Frequently Asked Questions

Why did my tax jump in my second year in Japan?

Because residence tax is charged on the previous year’s income and billed the following June. Your first year often has little or no residence tax (there was no prior-year Japanese income), so year two—when last year’s earnings catch up with you—feels like a sudden jump. It’s not a mistake; it’s the timing.

Do I have to file a tax return if I’m a regular employee?

Usually no. Your employer’s year-end adjustment settles your income tax. You only need to file a 確定申告 if you’re self-employed, have side income over ¥200,000, earn over ¥20 million, have multiple employers, or want to claim deductions like large medical expenses or furusato nozei without the one-stop system.

Is my income from my home country taxed in Japan?

For your first five years (as a “non-permanent resident”), foreign-source income is generally taxed only if you pay it into or remit it to Japan—money kept abroad usually isn’t. After more than five years in the last ten, you’re taxed on worldwide income. Tax treaties may reduce double taxation, so get professional advice for foreign salary, investments, or property.

When and how do I pay income tax from my return?

Income tax from your 確定申告 is due by the filing deadline, around March 15, and you pay it yourself—no slip arrives later. You can pay by bank transfer, at a convenience store, by credit card, or set up direct debit (振替納税), which delays the withdrawal to about late April. Filing and paying happen together.

What happens to my taxes if I leave Japan?

You still owe residence tax on the prior year’s income if you were resident on January 1. Appoint a tax representative (納税管理人) to receive and pay your bills after you go, and settle your income tax before leaving via an early return or through that representative.

The Bottom Line

Most of Japan’s tax system runs quietly in the background: withheld from your salary, reconciled at year-end, invisible. The part that trips people up isn’t complexity—it’s timing. Remember that residence tax always reflects last year, that income tax from a return is paid on the spot rather than billed later, and that your first five years may spare your overseas income, and you’ve understood more than most residents ever bother to. Set aside a little for the year-two bill, keep your My Number handy each February, and when your situation gets genuinely complicated, hand it to a zeirishi. For the wider picture of banking, payments, and daily money, see our guide to money in Japan, and for pension and health-insurance premiums—which sit alongside tax on your payslip—our guide to social insurance in Japan.

5 thoughts on “Taxes in Japan: An Expat’s Guide to Income Tax, Residence Tax & Filing (2026)”