Can foreigners buy property in Japan? Yes—and more easily than almost anywhere else. There’s no citizenship rule, no visa requirement, and no “permission to buy” step. A tourist could technically sign for a Tokyo apartment. The catch isn’t the buying; it’s everything around it: financing, the all-Japanese paperwork, the taxes nobody warned you about, and a 2026 reporting rule that recently caught a lot of overseas buyers off guard.

This guide walks through the whole thing from a resident’s point of view—who can buy, how the process actually goes step by step, what it really costs, how financing works, and the legal bits you can’t skip. I’m a lawyer based in Japan, so I’ll flag the things that genuinely matter and the things people overthink. (Standard caveat: this is general information for getting oriented, not legal or tax advice for your specific situation. For a real transaction, lean on a licensed agent, a shihō-shoshi, and a tax accountant.)

Can Foreigners Buy Property in Japan?

Short answer: yes. Japan places almost no restrictions on foreign ownership of real estate. You buy land and buildings on the same legal footing as a Japanese national, with full freehold ownership—not a leasehold, not a 99-year arrangement. Your visa status doesn’t gate ownership either. Permanent resident, work-visa holder, or someone who has never set foot here: all of you can legally hold title.

Where residency status does matter is financing. Owning is open to everyone; borrowing yen from a Japanese bank is where the questions start. More on that below.

Two oversight frameworks exist, and it’s worth knowing they’re monitoring rules, not ownership bans:

- Foreign exchange reporting (FEFTA). Non-residents who buy Japanese property must file a short post-purchase report. As of April 1, 2026, this applies to all purchases, including homes you’ll live in. Details in the non-resident section below.

- Security-sensitive land (the “Important Land” law, 重要土地等調査法). If a plot sits within roughly 1 km of a Self-Defense Force base, a nuclear plant, the coast guard, or certain border islands, the government can monitor how it’s used, and buyers of larger plots in the strictest zones may need to notify the Cabinet Office in advance. In 2026 the designated zones were expanded to include more ports and coastal areas. It applies to Japanese and foreign buyers alike, and for a typical city apartment it simply won’t come up.

If you’re curious how Japan compares globally, this overview of countries that restrict foreign buyers is a useful reality check—Japan is on the open end of the spectrum.

The Real Question: Are You Ready to Be Tied to Japan?

Before the mechanics, the honest part. The biggest barrier I see for foreign buyers isn’t legal or financial—it’s commitment. Buying a home quietly decides that you’re staying. Selling a Japanese property, especially an older one, isn’t quick or always profitable, so a purchase tends to lock you into the country for years in a way a lease never does. That’s a heavy thing to sign up for when “maybe we’ll move back” is still on the table.

That’s probably why, among the foreign families we know, very few bought as young singles or fresh arrivals. The common trigger is a child. Once a kid is in the picture—school catchment areas, wanting a stable base, the sense that you’re here for the long run—buying suddenly makes sense, and the same people who swore they’d never tie themselves down start touring apartments. If you’re feeling that pull, you’re in good company. If you’re not sure yet, there’s no shame in renting longer; Japan’s rental market is comfortable and there’s no penalty for waiting.

The Step-by-Step Process of Buying a Home in Japan

Here’s how a typical purchase unfolds. Most of it happens through a real estate agent (fudōsan-gaisha), who acts as the intermediary and walks you through the formalities. From first viewing to handover, three to four months is normal; longer if your loan needs extra review.

1. Set your budget and check financing first

Don’t fall for a property before you know what a bank will lend you. Get a rough pre-assessment early, because your residency status and income shape your real budget. Remember that the loan covers the property—you’ll need cash on hand for the purchase costs, commonly 6–10% of the price (broken down later). Build that into your number from day one.

2. Search for properties

The big listing portals are SUUMO, LIFULL HOME’S, and at home. They’re in Japanese, but browsable with a translation tool, and the same listings circulate across agencies. If your Japanese is limited, look for an agency that markets to international buyers—several Tokyo firms run full English service. Decide early what you’re after: a mansion (the Japanese word for a concrete condo, not a grand house), a detached house (ikkodate), or land to build on.

3. Viewings (naiken)

Found something promising? Ask the agent whether it’s still available, then book a viewing (naiken) by appointment. Go in person if you can. Check water pressure, mobile signal, morning light, the noise from the road, and how the building is maintained—the common areas of a mansion tell you a lot about how well the management association runs things.

4. Make an offer (kaitsuke)

When you’re ready, you submit a purchase application (kaitsuke shōmōsho) stating your price and conditions. Some price negotiation is normal, particularly on pre-owned homes that have been listed a while. This isn’t yet binding—it opens the conversation with the seller.

5. Explanation of important matters (jūyō jikō setsumei)

Before you sign anything, a licensed broker must read you the jūyō jikō setsumei—a formal disclosure of the property’s legal and physical facts: boundaries, building restrictions, the management association’s finances, any defects. It’s dense and delivered in Japanese. This is the single document I’d never wave through. If your Japanese isn’t strong, arrange a translation or bring someone fluent; this is where problems hide.

6. Sign the contract and pay the deposit

You sign the sales contract (baibai keiyaku) and pay an earnest-money deposit (tetsuke-kin), typically 5–10% of the price. The tetsuke has teeth: if you walk away without cause, you forfeit it; if the seller backs out, they generally owe you double. Make sure the contract includes a loan contingency (rōn tokuyaku) so you can cancel and recover your deposit if your mortgage falls through.

7. Finalize your mortgage

With a signed contract, you complete the formal loan application. Approval can take a few weeks. The forms are detailed and almost entirely in Japanese, so this is the moment to lean on an English-capable bank or your agent. See our full guide to getting a home loan in Japan as a foreigner for who qualifies, which banks lend to non-PR holders, and current rates.

8. Settlement and registration (kessai & tōki)

On settlement day, the loan funds, you pay the balance, and a shihō-shoshi (judicial scrivener) registers the ownership transfer at the Legal Affairs Bureau on the spot. You get the keys. From here it’s the usual move-in admin—utilities, address change, and the rest. Our moving timeline and checklist covers that stretch.

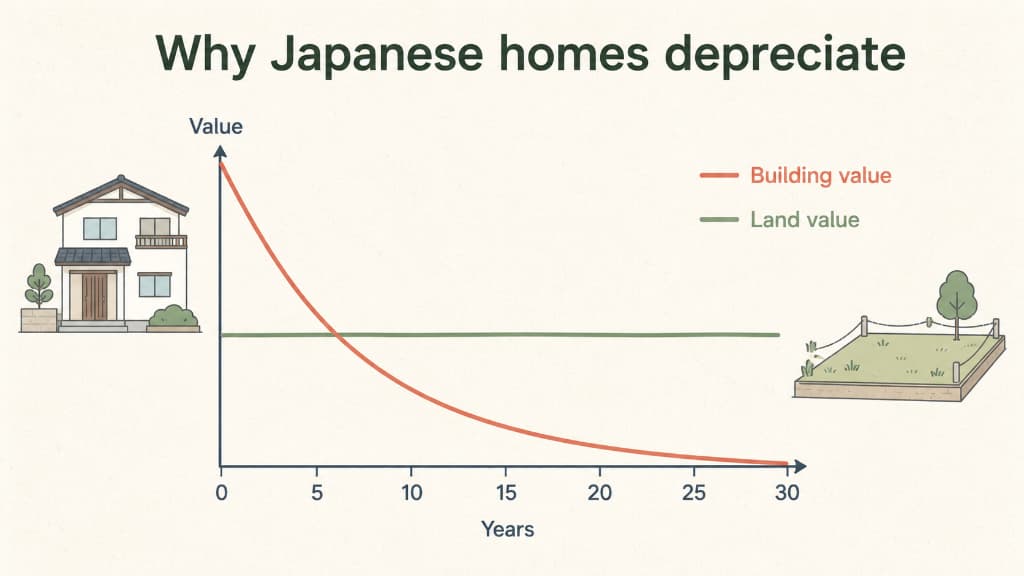

New vs. Used, and Why Old Houses Are Almost Free

One thing that surprises buyers from abroad: in Japan, buildings depreciate while land holds its value. A wooden house is often treated as having little to no value after about 20–30 years, regardless of condition. The land underneath is what you’re really buying. This is the opposite of the “homes always appreciate” instinct many expats arrive with, and it changes how you think about a purchase.

Practical takeaways: a brand-new mansion carries a premium that drops the day you move in, much like a new car. A well-built used mansion in a good location can be the sweet spot. And those eye-catchingly cheap detached houses? Much of the price is land—the building is thrown in at near zero—so factor in renovation. Don’t buy a home here expecting it to be an appreciating asset; buy it because you want to live in it.

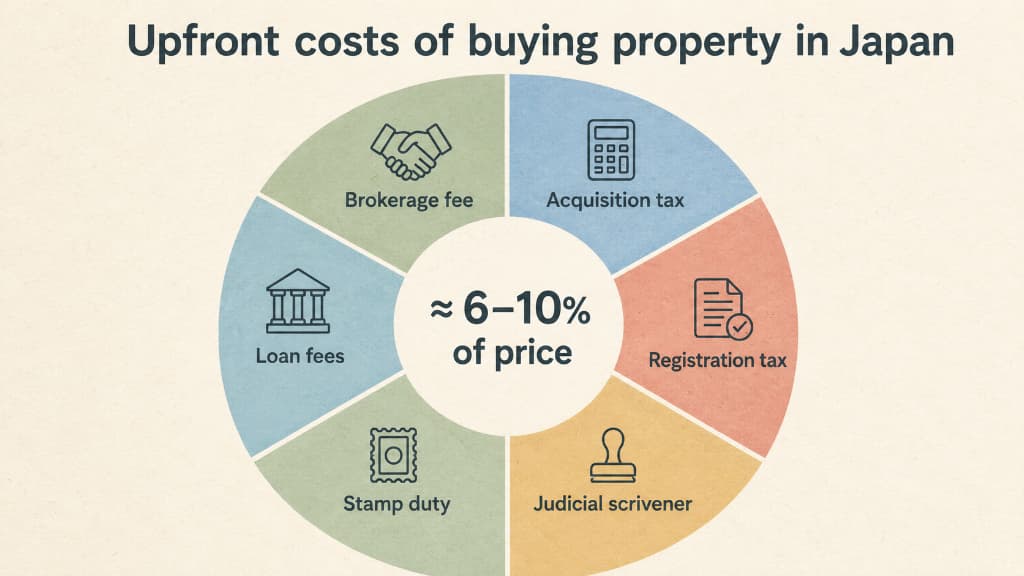

Costs and Taxes: What Buying Really Adds Up To

The sticker price is not the price. Budget roughly 6–10% of the purchase price in one-time costs on top, payable in cash around closing. Underestimating this is the classic first-timer mistake. Here’s the breakdown:

| Cost | Roughly how much | What it is |

|---|---|---|

| Agent brokerage fee | 3% of price + ¥60,000 + 10% tax (legal cap) | The largest single cost; the legal maximum for a sale |

| Real estate acquisition tax (不動産取得税) | ~3–4% of assessed value | One-time tax billed a few months after purchase; assessed value is usually well below market price |

| Registration & license tax (登録免許税) | ~0.4–2% of assessed value | Paid to register the ownership transfer (and the mortgage); reduced rates apply to qualifying homes |

| Judicial scrivener fee (司法書士) | ~¥100,000–200,000 | The shihō-shoshi who handles registration |

| Stamp duty (印紙税) | ~¥10,000–60,000 | Revenue stamp on the contract; depends on price (reduced rates currently apply) |

| Loan-related fees | Varies | Guarantee fee, administration fee, mortgage registration |

Note the correction many older guides get wrong: it’s real estate acquisition tax, not “income tax”—a one-time levy on acquiring property, calculated on the assessed value, not what you paid.

Then there are the ongoing costs you’ll pay every year as an owner:

- Fixed asset tax (固定資産税) and, in urban areas, city planning tax (都市計画税)—together usually around 1.4–1.7% of assessed value per year, billed by your municipality.

- Management fees and a repair reserve (修繕積立金) if you buy a mansion—monthly payments to the building’s management association. Check these before you buy; an underfunded reserve can mean a nasty special assessment later.

Financing: Can a Foreigner Get a Mortgage?

This is the real hurdle, so I’ll keep it short here and point you to the deep dive. Japanese mortgages come with famously low rates and a built-in perk: group credit life insurance (dan-shin, 団体信用生命保険), which pays off the remaining balance if the borrower dies, so your family keeps the home free and clear.

Approval is easiest if you have permanent residency or a Japanese spouse. Without PR it’s still very doable—banks like SMBC Trust and Shinsei (and others) lend to foreign residents—but expect to show stable employment, tax payment, and residency in Japan, and possibly a larger down payment. For the full picture of who qualifies, which banks to approach, current interest rates, and the application steps, read our dedicated home loan guide for foreigners in Japan.

Registration: Putting the Property in Your Name

After purchase, ownership is recorded in the public real estate registry (tōki). Anyone—foreigner or not, resident or not—can be registered as owner. Buy through an agent and the process is handled for you; the shihō-shoshi does the actual filing at settlement.

Why it matters so much: under Japanese law, registration is what protects your ownership against third parties (Civil Code Art. 177). In theory, an unregistered buyer can be defeated by someone who registers first—so registration isn’t a formality to put off, it’s the thing that makes the property truly yours. It’s also why buying directly from a seller without professional help is risky; if you go that route, hire a shihō-shoshi or lawyer.

Registration needs documents like a registered seal certificate (inkan shōmeisho) and residence certificate (jūminhyō). Short-term residents (under three months) who can’t get these can usually obtain an equivalent affidavit from their home country’s embassy in Japan.

Buying From Abroad? The 2026 Reporting Rule and Non-Resident Notes

This section is for non-residents—broadly, people buying from overseas rather than living here. (Under the foreign exchange rules you generally count as a “resident” once you’re working in Japan or six months have passed since you entered, so most expats actually living here fall outside this report.)

The important change: under the Foreign Exchange and Foreign Trade Act (FEFTA), a non-resident who acquires Japanese real estate must file a report (Form 22) with the Minister of Finance via the Bank of Japan, within 20 days of the acquisition. Until recently, property bought purely as a personal or family residence was exempt. That exemption was abolished as of April 1, 2026: now every acquisition by a non-resident must be reported, regardless of purpose. It’s a notification, not a permission—but it’s mandatory, so don’t let it slip. (If you’re buying from abroad, confirm the current procedure with the Ministry of Finance or your advisor before you file, as the post-2026 forms are new.)

Two more things that catch overseas buyers and investors:

- Moving money in and out. Large international transfers trigger identity checks, and carrying cash or near-cash worth more than ¥1 million out of Japan requires a customs declaration. For sending funds, Wise usually beats banks on exchange and transfer fees.

- Tax on rental income. If you rent the property out, the income is taxable in Japan—income tax, plus resident tax if you’re a resident, and possibly enterprise tax. A non-resident landlord typically appoints a tax agent (nōzei kanrinin) in Japan to handle filings.

Buy or Keep Renting?

Circling back to where we started: buying makes the most sense when you’re confident you’re staying, ideally five-plus years, and you value stability over flexibility—which is exactly why so many foreign families buy once kids and schools enter the picture. If your future in Japan is still open-ended, renting keeps your options alive and spares you the depreciation, the acquisition tax, and the hassle of selling an older building. If you’re weighing the rental side, see our guides on renting an apartment in Japan and what’s really in a Japanese rental contract.

Frequently Asked Questions

Can a foreigner buy property in Japan without permanent residency or a visa?

Yes. There’s no visa or residency requirement to own real estate in Japan—even non-residents living abroad can buy. The restriction people imagine doesn’t exist. What’s harder without permanent residency is getting a mortgage, not the ownership itself.

How much money do I need on top of the purchase price?

Budget around 6–10% of the price in one-time costs—brokerage fee, acquisition tax, registration and license tax, judicial scrivener, stamp duty, and loan fees—payable in cash near closing. After that, expect annual fixed asset tax (and city planning tax), plus monthly management and repair fees if it’s a mansion.

Is Japanese property a good investment?

Treat it as a place to live, not a growth asset. Buildings generally depreciate while land holds value, so most homes don’t appreciate the way they might back home. Central-city land and well-located used mansion units hold value best; older detached houses are mostly a land play.

Do I have to report my purchase to the government?

If you’re a non-resident buying from abroad, yes—a FEFTA report (Form 22) to the Bank of Japan within 20 days, for any purpose since April 1, 2026. If you live in Japan and count as a resident under the foreign exchange rules, this particular report generally doesn’t apply to you.

How long does the buying process take?

From the property you like to keys in hand, plan on roughly three to four months: viewing and offer, the important-matters explanation and contract, mortgage approval, then settlement and registration. A complex loan review or a slow seller can stretch it.

A Recommended Read

If you want to go deeper on buying real estate in Japan from a foreigner’s perspective, “Landed Japan: Key Local Knowledge You Need to Buy Japanese Real Estate” is thorough and practical. The author has been a Hong Kong–based investor in Tokyo property since 2010, so it’s written from real experience.

And for the wider settling-in picture, see our moving checklist and our practical guide to managing money in Japan.

One thought on “Buying Property in Japan as a Foreigner: Process, Costs & 2026 Rules”